Our lives are defined by numbers: your date of birth, your phone number and your Social Security number, to name just a few. But what about your credit score?

This simple three-digit number also plays a significant role, especially in your financial life. That’s because it largely determines your access to credit and, thus, your ability to buy a home or a car and to start a business, among other things—and how much you’ll have to pay for them.

Maybe you’re thinking: “I don’t need to worry about my credit score; I already have a house.” Or “I use a debit card or pay cash for everything, so my credit score doesn’t matter.” More than a third (36 percent) of young Americans between the ages of 18 and 29 have never used a credit card, according to CreditCards.com.

Fair enough, but you still want good credit—and here’s why: The world uses credit scores to make decisions about more than just lending money. For example, let’s say you want to rent an apartment. Your prospective landlord is likely to run a credit check on you to make sure you have a good history of paying your bills. Insurance companies use your credit score to determine how much to charge you for auto insurance. And some employers even check the credit scores of job applicants, along with references, work history and interview performance, before extending an offer for certain positions.

How Is Your Credit Score Determined?

The most widely used credit scoring system was developed by Fair Isaac Corporation and is called the FICO®score. FICO scores range from 300 to 850. Generally, the higher the number, the more likely you are to qualify for a loan and the better the terms and interest rates you may receive—and the more money you may save in financing a car, a mortgage or another large purchase. To see how much, consider the following chart. Using data from the Loan Savings Calculator at myFICO.com, it illustrates how your credit score impacts how much it would cost you to borrow $150,000 to buy a house using a 30-year fixed mortgage (data as of July 13, 2015; rates change daily).

- Credit score: 760-850/ 3.782% interest rate/ $697 per month mortgage

- Credit score: 620-639/ 5.371% interest rate/ $840 per month mortgage

As you can see, although the 1.589 percent difference in rates may seem small, the lower credit score would cost you $140 a month more for your mortgage ($823 – $683). That’s an extra $51,186 in interest payments over the life of your home loan.

Money Management Matters

What can you do to ensure your credit rating is as high as possible? A good credit score starts with smart spending, including the following:

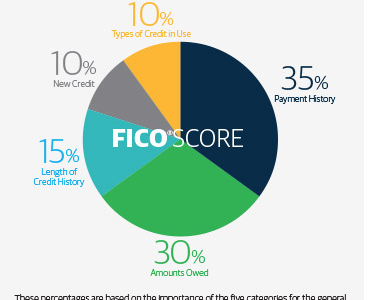

- Pay your bills on time, every time. As the chart below illustrates, your payment history makes up 35 percent of your FICO score and is the most influential factor in your credit report.

- Get the best credit card you can. A list of currently available credit card deals by credit score is available on myFICO.com.

- Avoid applying for excessive credit. Opening a bunch of credit cards in a short period of time shows up as a “hard hit” on your credit report. Those types of inquiries can potentially lower your score.

- Stay well under your credit limit, and charge only what you can afford. The amount of debt you carry accounts for 30 percent of your FICO score. If you use too much of the credit available to you, it could damage your score.

- Keep your no-fee credit cards open, even if you’re not using them. The longer you hold your card, the better your credit score will be because lenders can see that you have a good history of repaying your debt.

- Don’t use prepaid debit cards—they don’t help you build credit and often carry high fees.

- Check your credit report annually. Mistakes in credit reports happen more often than you might think, so you’ll want to check your credit report regularly and report any errors or discrepancies immediately. Federal law entitles you to one free copy of your credit report every 12 months from each of the three main credit bureaus—Equifax®, TransUnion® and Experian®. You can view your free credit reports at AnnualCreditReport.com. And keep in mind, requesting a copy of your credit report won’t impact your credit score in any way.

Bottom line: Good credit management leads to higher credit scores. This can lower your cost to borrow and put more money in your pocket to save and invest. It also means you’ll have access to the financing you need, whenever you need it.